每个月的最后一天都会做个目录,方便自己也方便大家~

2018年12月:

我的2018年投资成绩

我的2014年投资成绩

PANAMY最新季度报告

当年我迅速累积身家的3把武器

2018年11月:

HARTALEGA最新季度财政报告

2018年篇:长期投资的后果

AEONCR最新季度财政报告

等啊等,股市风暴何时来?

2018年10月:

AEON 2018年第2季度财政报告

2018年9月:

我的2018年第3季度投资成绩

投资界里的独角兽

2018年8月:

PANAMY 2018年年度报告+第1季财政报告

我的2013年投资成绩

2018年7月:

LPI 2018年第2季度财政报告

扮演受害者倾向

AEONCR 2018年度报告+2019第1季度财政报告

掌控情绪VS被情绪掌控

PANAMY 2018年第4季度财政报告

2018年6月:

我的2018年上半年投资成绩

AEONCR 2018年股东大会

为了获胜 VS 避免失败 Part.2

COCOLAND 2017年度财政报告

为了获胜 VS 避免失败

向作家之路又迈进了一步

2018年5月:

AEON 2017年度财政报告+2018第1季度财政报告

最近的心情..........

大选之后的第一个股票交易日

HUPSENG 2017 年度财政报告

一个大家都忽略了的买股成本

2018年4月:

OFI 2018年第3季度财政报告

COCOLAND 2017年第4季度财政报告

小刀锯大树

NESTLE 2017年度财政报告

PBBANK的海外业务

我面对大选的投资策略

我的2018年第1季度投资回酬

2018年3月:

造神论

AEON 2017年第4季度财政报告

我的2012年投资成绩

PANAMY 2018年第3季度财政报告

一股致富!

2018年2月:

NESTLE 2017年第4季度财政报告

HUPSENG 2017年第4季度财政报告

F&N 2018年第1季度财政报告

HARTALEGA 2018年第3季度财政报告

我如何解释我的投资

在股票投资上ALL IN

2018年1月:

股价上涨的要素

OFI 2018年第2季度财政报告

其实我讨厌红股与拆细

F&N 2017年度财政报告

我的投资回酬计算方式(ROE & ROA)

我的2017年投资成绩

我的脸书专页

我的推特:@TheCellist86

Monday, 31 December 2018

List of articles of January~December 2018

I will make a list of articles every last day of the month,

so that is easier for me and for everyone to refer~

December 2018:

My investment return for year 2018

My investment return for year 2014

PANAMY latest financial report

My 3 weapons in shares market

November 2018:

HARTALEGA latest financial report

Year 2018 version: the consequence of long term investment

AEONCR latest financial report

Waiting and waiting, when will the stock market crashes?

October 2018:

AEON 2nd quarter 2018 financial report

September 2018:

My investment return for 3rd quarter of year 2018

UNICORN in investment world

August 2018:

PANAMY annual report 2018 + 1st quarter financial report

My investment return for year 2013

July 2018:

LPI 2ndquarter 2018 financial report

Enjoy being the victim

AEONCR 2018 annual report + 1st quarter report

Investing and emotional control

PANAMY 4th quarter 2018 financial report

June 2018:

My investment return for 1st half of 2018

AEONCR AGM 2018

To win or not to lose part2

COCOLAND annual report 2017

To win or not to lose

A step closer for becoming a writer

May 2018:

AEON 2017 annual report + 1st quarter 2018 financial report

Some thoughts lately........

The 1st shares trading day after G.E.

HUPSENG annual report 2017

The cost of investment is much higher than we thought

April 2018:

OFI 3rd quarter 2018 financial report

COCOLAND 4th quarter 2017 financial report

Cutting down trees by using a small knife

NESTLE annual report 2017

Oversea business of PBBANK

My investment strategy for upcoming General Election

My investment return for 1st quarter 2018

March 2018:

Human tendency and idolization

AEON 4th quarter 2017 financial report

My investment return for year 2012

PANAMY 3rd quarter 2018 financial report

Diversification VS Focused Investing

February 2018:

NESTLE 4th quarter 2017 financial report

HUPSENG 4th quarter 2018 financial report

F&N 1st quarter 2018 financial report

HARTALEGA 3rd Quarter 2018 Financial Report

How did I explain my investment

ALL IN!!! At shares investment

January 2018:

Important factors of share price rising

OFI 2nd Quarter 2018 Financial Report

Actually I don't like Bonus Issue & Share Split

F&N Annual Report 2017

How I calculated my investment return(ROA & ROE)

My investment return for year 2017

so that is easier for me and for everyone to refer~

December 2018:

My investment return for year 2018

My investment return for year 2014

PANAMY latest financial report

My 3 weapons in shares market

November 2018:

HARTALEGA latest financial report

Year 2018 version: the consequence of long term investment

AEONCR latest financial report

Waiting and waiting, when will the stock market crashes?

October 2018:

AEON 2nd quarter 2018 financial report

September 2018:

My investment return for 3rd quarter of year 2018

UNICORN in investment world

August 2018:

PANAMY annual report 2018 + 1st quarter financial report

My investment return for year 2013

July 2018:

LPI 2ndquarter 2018 financial report

Enjoy being the victim

AEONCR 2018 annual report + 1st quarter report

Investing and emotional control

PANAMY 4th quarter 2018 financial report

June 2018:

My investment return for 1st half of 2018

AEONCR AGM 2018

To win or not to lose part2

COCOLAND annual report 2017

To win or not to lose

A step closer for becoming a writer

May 2018:

AEON 2017 annual report + 1st quarter 2018 financial report

Some thoughts lately........

The 1st shares trading day after G.E.

HUPSENG annual report 2017

The cost of investment is much higher than we thought

April 2018:

OFI 3rd quarter 2018 financial report

COCOLAND 4th quarter 2017 financial report

Cutting down trees by using a small knife

NESTLE annual report 2017

Oversea business of PBBANK

My investment strategy for upcoming General Election

My investment return for 1st quarter 2018

March 2018:

Human tendency and idolization

AEON 4th quarter 2017 financial report

My investment return for year 2012

PANAMY 3rd quarter 2018 financial report

Diversification VS Focused Investing

February 2018:

NESTLE 4th quarter 2017 financial report

HUPSENG 4th quarter 2018 financial report

F&N 1st quarter 2018 financial report

HARTALEGA 3rd Quarter 2018 Financial Report

How did I explain my investment

ALL IN!!! At shares investment

January 2018:

Important factors of share price rising

OFI 2nd Quarter 2018 Financial Report

Actually I don't like Bonus Issue & Share Split

F&N Annual Report 2017

How I calculated my investment return(ROA & ROE)

My investment return for year 2017

My Twitter : @TheCellist86

我的2018年投资成绩

不知不觉,又平平安安(?)地度过了一年。

今年的投资回酬呢,ROA为13.3%,ROE为16.0%。

与前两年的回酬比起来,

今年的回酬巴仙率少了很多,

心情难免有点失落..........

接下来对比看看2018年头和年尾的投资组合,

2018年一开始时,

我的投资组合如下:

1) AEONCR (30%)

2) LPI (22%)

3) NESTLE (15%)

4) PANAMY (12%)

5) PBBANK (6%)

6) F&N (5%)

7) 其他如COCOLAND, DLADY, HARTA, HUPSENG (共10%)

2018年年尾时:

1) AEONCR (31%)

2) HARTA (21%)

3) LPI (17%)

4) PANAMY (12%)

5) PBBANK (8%)

6) AEON (7%)

7) NESTLE (4%)

今年的投资回酬,主要得感谢以下3家公司:

AEONCR从RM13.46 涨到RM15.30。

NESTLE从RM103.20涨到RM147.40。

PBBANK从RM20.78涨到RM24.76。

只可惜NESTLE和PBBANK占组合比例不大,

所以不能明显地拉高回酬。

除此以外,

我也在RM33-RM36之间出清F&N,

然后清理了一下组合,

只留下我觉得还有投资价值的。

在这里顺便写下历年的投资成绩:

2011 : ROE = +28.0%

2012 : ROE = +32.8%

2013 : ROE = +15.0%, ROA = +13.3% (开始使用SMF)

2014 : ROE = -12.0%, ROA = - 8.0%

2015 : ROE = +21.6%, ROA = +13.3%

2016 : ROE = +38.0%, ROA = +22.2%

2017 : ROE = +40.5%, ROA = +24.9%

2018 : ROE = +16.0%, ROA = +13.3%

如果2011年当初我有一百万,

那么经过8年的投资后,

会成长至470万左右,

年复利为21.3%.

如今我的资金规模,所投入的本钱只有7%,SMF占了33%,其余60%都是盈利。

简化地说,

假设如今我的资金规模为100千,

这100千里面,7千是我真正投入的本钱,

另外33千是SMF借来的,

而剩下的60千都是股市上涨得来的盈利。

以上就是今年的投资成绩总结。

2019年嘛........

只希望身体健健康康的,

毕竟今年有接近4个月时间都在痛症中度过.....

投资就是自己思考,自己做决定。

感谢阅读。

以上言论没有任何买卖建议,

大家买卖自负。

大家买卖自负。

我的2014年投资成绩

PANAMY最新季度财政报告

当年我迅速累积身家的3把武器

HARTALEGA最新季度财政报告

长期投资的后果(2018年篇)

其他链接:

2018年文章目录

2017年文章目录

我的2017年投资成绩

关于本人

我的脸书专页

我的推特:@TheCellist86

My investment return for year 2018

Finally is the end of year 2018,

this year my investment return: ROA is 13.3%, ROE is 16.0%.

Comparing with the last two years,

this year my return was significantly lower,

so I kinda feeling down right now......

Below is the comparison of my investment portfolio at the start and end of year 2018:

Start of year 2018:

1) AEONCR (30%)

2) LPI (22%)

3) NESTLE (15%)

4) PANAMY (12%)

5) PBBANK (6%)

6) F&N (5%)

7) Others like COCOLAND, DLADY, HARTA, HUPSENG (totally 10%)

End of year 2018:

1) AEONCR (31%)

2) HARTA (21%)

3) LPI (17%)

4) PANAMY (12%)

5) PBBANK (8%)

6) AEON (7%)

7) NESTLE (4%)

This year my investment return were mainly contributed by these three companies:

AEONCR which rose from RM13.46 to RM15.30.

NESTLE from RM103.20 to RM147.40。

PBBANK from RM20.78 to RM24.76。

Sadly that NESTLE and PBBANK took up a small portion of my portfolio,

so didn't contribute a significant return.

On the other hand,

I sold all my F&N between RM33-RM36,

also I did some cleaning on my portfolio and downsized to 7 companies only.

My investment return for the past few years:

2011 : ROE = +28.0%

2012 : ROE = +32.8%

2013 : ROE = +15.0%, ROA = +13.3% (started using SMF)

2014 : ROE = -12.0%, ROA = - 8.0%

2015 : ROE = +21.6%, ROA = +13.3%

2016 : ROE = +38.0%, ROA = +22.2%

2017 : ROE = +40.5%, ROA = +24.9%

2018 : ROE = +16.0%, ROA = +13.3%

If I have 1 million at the start of year 2011,

after 8 years of investment,

it would have grown into around 4.7 million,

annual compound interest is 21.3%.

Currently out of my total investment capital,

7% of it was the actual money I put into,

33% is SMF,

the rest 60% was all the profit.

For example,

if the value of my investment portfolio is 100K,

then 7K is the actual money I put into it,

33K is from SMF,

60K is the profit I accumulated from share market.

That's all for the conclusion of my investment return for year 2018,

As for year 2019,

I just hope that my body still continue to stay healthy,

since for 4 months long in year 2018 I was in pain.............

Investment is about doing own thinking, making own decision.

Thanks for reading.

I don't provide any buying/selling suggestion above,

please make your own investment decision and be responsible with it.

please make your own investment decision and be responsible with it.

Recent articles :

My investment return for year 2014

PANAMY latest financial report

The three weapons

HARTALEGA latest financial report

Year 2018 version:the consequence of long term investment

Other links:

List of articles of year 2018

List of articles of year 2017

My investment return for year 2017

My self-introduction article

My Twitter : @TheCellist86

Saturday, 22 December 2018

我的2014年投资成绩

这个部落格,

不只是用来记录和写下现在的一切,

也是用来回顾我过去的投资,

所以今天就来写下我以前2014年的投资成绩,

也是我迈入投资的第4年。

我在2014年1月1日的投资组合:

1)AEON

2)AEONCR

3)DLADY

4)NESTLE

5)PANAMY

6)PBBANK

而我在2014年12月31日的投资组合:

1)AEON

2)AEONCR

3)DLADY

4)NESTLE

5)PANAMY

6)PBBANK

7)LPI

当年的回酬:ROA=-8.0%, ROE=-12.0%

没错,

是负回酬,

我在那年的投资蒙受了损失。

投资的负回酬主要归功于:

AEONCR从RM14.72跌到RM12。(当年股价,跟现在红股后的价钱不能对比。)

DLADY从RM47.14跌到RM42.40。

PANAMY从RM22.32跌到RM18.50。

当年,

我开始累积LPI,

根据现在红股后的股价来看,

我累积在RM9到RM10之间。

现在看回来,

我应该累积当时股价才RM68.50的NESTLE才对.....................

当年,

也是我投资亏损的一年。

而且因为SMF的放大,

从亏损8%被放大到亏损12%.

不要觉得从8%到12%很小,

试想一想要是亏了80%后放大到120%,

到时简直不只亏到渣都不剩,

还欠钱呢!

当然,

就像车祸后,不能从此不驾车上路。

同样道理,

我依然继续使用SMF,但用得更加小心~

而且因为2014年的大跌,

投资机会到处浮现,

我才得以在接下来的2015年翻身.........

感谢阅读。

以上言论没有任何买卖建议,

大家买卖自负。

大家买卖自负。

PANAMY最新季度财政报告

当年我迅速累积身家的3把武器

HARTALEGA最新季度财政报告

长期投资的后果(2018年篇)

AEONCR最新财政报告

其他链接:

2018年文章目录

2017年文章目录

我的2017年投资成绩

关于本人

我的脸书专页

我的推特:@TheCellist86

My investment return for year 2014

This blog is not only for writing and recording down what is happening now,

but also to review my past investment,

so today I will write down my investment return of year 2014,

which was the 4th year I started to invest.

My investment portfolio at 1st January 2014:

1)AEON

2)AEONCR

3)DLADY

4)NESTLE

5)PANAMY

6)PBBANK

My investment portfolio at 31st December 2014:

1)AEON

2)AEONCR

3)DLADY

4)NESTLE

5)PANAMY

6)PBBANK

7)LPI

My investment return for year 2014: ROA=-8.0%, ROE=-12.0%.

Yes,

negative return,

I lost money that year.

The negative return was mainly contributed by:

AEONCR which dropped form RM14.72 to RM12. (Shares price that time, can't compare with the current price since after bonus issue.)

DLADY dropped from RM47.14 to RM42.40.

PANAMY dropped from RM22.32 to RM18.50.

At the same year,

I started to accumulate LPI around RM9-RM10 (this one can compare with current shares price since it was adjusted after bonus issue.)

Looking back from now,

I should had accumulated NESTLE at RM68.50 instead.............

That year,

I lost money through investment.

Because of the leverage effect of SMF,

my loss of 8% was magnified to 12%.

Please don't think from 8% to 12% is small,

imagine if it was a loss of 80%?

Then it will be magnified to 120%!

Not only lost everything,

but owing the bank some more!

Well.........

Just because we had accident on the road,

doesn't mean we shouldn't drive.

So I still continue to use SMF,

just that now I am more careful of using it.

Because of the bear market at year 2014,

there were some investment opportunities started to appear,

that was why I was able to rise again at year 2015.........

Thanks for reading.

I don't provide any buying/selling suggestion above,

please make your own investment decision and be responsible with it.

please make your own investment decision and be responsible with it.

Recent articles :

PANAMY latest financial report

The three weapons

HARTALEGA latest financial report

Year 2018 version:the consequence of long term investment

AEONCR latest financial report

Other links:

List of articles of year 2018

List of articles of year 2017

My investment return for year 2017

My self-introduction article

My Twitter : @TheCellist86

Thursday, 13 December 2018

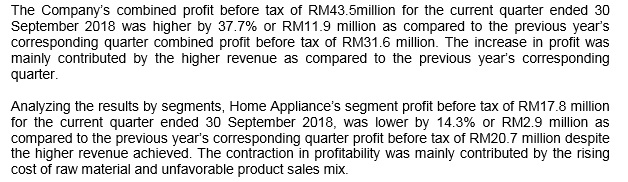

PANAMY最新季度财政报告

今天来看看PANAMY在11月尾出炉的财政报告。

首先:

营业额和盈利比起去年同季进步很多,

真是令人开心~

不过这一季营业额增加那么多是有原因的...........

稍后就会提到。

然后业务方面:

但Home Appliance的盈利就没去年那么好看了......

各地的业务:

当然,

这是有原因的...........

就像下面所提到的,

本地营业额增加是因为零GST到8月31日为之,

所以很多商家和消费者都选择在这一季买入PANAMY的产品。

主要是中东和越南市场的需求下滑。

盈利方面,

主要都是跟着营业额的增加而水涨船高。

管理层的展望:

公司接下来似乎要着重于降低成本。

最后是人见人爱的股息:

每年都是每股15 sen~

季度报告就到此为止,

觉得不详细的话欢迎去Bursa网站下载来看。

至于PANAMY是不是还值得继续持有呢?

投资就是自己思考,自己做决定。

感谢阅读。

以上言论没有任何买卖建议,

大家买卖自负。

大家买卖自负。

当年我迅速累积身家的3把武器

HARTALEGA最新季度财政报告

长期投资的后果(2018年篇)

AEONCR最新财政报告

等啊等,股市风暴何时来?

其他链接:

2018年文章目录

2017年文章目录

我的2017年投资成绩

关于本人

我的脸书专页

我的推特:@TheCellist86

PANAMY latest financial report

Today I would like to have a look at PANAMY's latest financial report which was released at end of Novemeber.

First:

Comparing with same quarter last year,

the revenue and profit improved a lot,

such a good news~

However there are reasons why was the revenue improved which will be mentioned later.........

For more details of the segment:

but the profit of Home Appliance business was not as good as last year............

Based on geographic:

of course,

there was a reason behind it...........

Just like what was mentioned at below,

a lot of dealers and consumers chose to buy more PANAMY products at this quarter since the zero GST was until 31st August only,

that was the reason why revenue in Malaysia improved so much.

The main reason of growing profit was because of the growth of revenue.

The outlook by management:

seems like the company will focus more on prudent cost management.

Lastly,

the dividend which everyone love:

That's all for the financial report,

if you thini it is not detailed enough,

feel free to go to Bursa website to download the report and read again.

As for whether is it still worthy to invest at PANAMY?

Investment is about doing own thinking, making own decision.

Thanks for reading.

I don't provide any buying/selling suggestion above,

please make your own investment decision and be responsible with it.

please make your own investment decision and be responsible with it.

Recent articles :

The three weapons

HARTALEGA latest financial report

Year 2018 version:the consequence of long term investment

AEONCR latest financial report

Waiting and waiting, when will the stock market crash?

Other links:

List of articles of year 2018

List of articles of year 2017

My investment return for year 2017

My self-introduction article

My Twitter : @TheCellist86

Wednesday, 5 December 2018

当年我迅速累积身家的3把武器

在阅读这篇文章之前,

建议先阅读我在2017年写过的:

为何我使用SMF来投资

这篇文章其实写于2014/2015年,

并发表在Investalks投资论坛里。

原本题目是<<东山再起>>,

就是假设说万一我一夜之间什么都没有了,

股本归零,

那么我需要多少时间才能东山再起呢?

发表了文章后,

我就被提醒,

其实我不需要重复以前做过的东西,

反而可以更快东山再起。

既然东山再起这个题目不适合,

那么就得另外想个适合的题目了。

反复读了文章后,

我决定把题目定为《当年我迅速累积身家的3把武器》,

让大家知道我是靠哪3样武器在股市里迅速累积身家。

当然,

这是基于我本人经验所写的,

并不是最好的,

毕竟我不是神。

至于文章里所提到的数字嘛,

看看就好~

那么,

文章就从这里开始:

为了迅速累积身家,

首先第1把武器就是高收入。

当年,

我就是不停地找客户,来提高收入,

好让我每个月可以存个RM3500。

第2把武器就是适当的投资回酬,

也就是大约每年15%。

第一年,

每个月存RM3500,

12个月后,我就会有12xRM3500 = RM42,000。

这一年也可以投质,

但因为一开始什么都没有,

就算回酬15%也不会很多,干脆忽略。

股本RM42,000,

就可以使用第3把武器,也就是SMF了。

(SMF = Share Margin Financing)

SMF不要太多,30%就好,也就是大约RM18,000。

如此一来,Asset=RM60,000 。

当中RM42,000是equity, RM18,000是debt。

第二年,

每个月再存RM3500,

那么就会再加多RM42,000的股本,身家6位数。

asset = RM102,000, 当中RM84,000是equity,RM18,000是debt。

然后投质回酬15%,

今年新加的股本别算,算去年的RM60,000就好。

0.15x60k = 9k, 投质赚了RM9000。

那么,Asset = RM111,000,

当中RM93,000是equity, RM18,000是debt。

身家多了后,

SMF也可以用更多,

但还是保持30%比例,

所以大约用SMF多RM22,000。

如此一来,Asset = RM133,000。

当中RM93,000是equity, RM40,000是debt。

第三年,

继续每个月再存RM3500,

那么就会再继续加多RM42,000的股本,净身家6位数。

Asset=RM175,000,

当中RM135,000是equity,RM40,000是debt。

然后投质回酬15%,

也是今年新加的股本别算,算去年的RM133,000就好。

0.15x133k = 20k左右, 投质赚了RM20,000。

那么,Asset = RM195,000,

当中RM155,000是equity, RM40,000是debt。

身家已经RM195,000了,

那么SMF多个RM5000,就是RM200,000了。

如果还要继续冲刺,

30%比例,那就SMF多RM25,000。

如此一来,Asset=RM220,000。

当中RM155,000是equity, RM65,000是debt。

当年,

我就是用高收入、适当的投资回酬和SMF这3把武器来累积身家。

当然,

这只是我个人的做法,并不适合其他人。

每个月存RM3500??

很多人喜欢自我催眠他们做不到。

SMF30% ??

很多人拒绝和害怕负债。

投质回酬15% ??

这个很多人应该可以接受,毕竟这几年没有什么大跌,大部分的人回酬还多过15% ~

以上就是我的3把武器。

各位闯入股市又有多少武器在手呢?

哪种武器最适合自己呢?

投资就是自己思考,自己做决定。

感谢阅读。

以上言论没有任何买卖建议,

大家买卖自负。

大家买卖自负。

HARTALEGA最新季度财政报告

长期投资的后果(2018年篇)

AEONCR最新财政报告

等啊等,股市风暴何时来?

AEON 2018年第2季度财政报告

其他链接:

2018年文章目录

2017年文章目录

我的2017年投资成绩

关于本人

我的脸书专页

我的推特:@TheCellist86

My 3 weapons in shares market

You are recommended to read this:

Why did I use SMF for my investment

before reading today's article.

This article was originally written at between year 2014 and 2015,

and published at Investalks forum.

The original title was different,

because I was intended to calculate how much time I need to re-accumulate the wealth I was having if out of a sudden I lost everything.

After publishing the article,

I was reminded that actually if I try not to repeat doing the same thing,

it might be faster for me to re-accumulate my wealth.

Since the original title was not suitable anymore,

of course I need to think a new title.

After reading my article again,

I decided to title it as "The three weapons that boosted my speed of accumulating wealth at shares market",

to share with everyone how did I accumulate my wealth at shares market for the first 3 years of my investment life.

Of course,

it was all based on my personal experience,

I am not God,

so it doesn't mean my experience was the best.

As for the numbers used in the article,

just a reference,

doesn't mean it is real.

So...........

Let's begin:

In order to accumulate wealth faster,

the 1st weapon is high income.

At the start of my investment life,

I kept on searching for customers to increase my income,

so that I was able to save RM3500 every month.

The 2nd weapon is reasonable return of investment,

around 15% every year.

1st year,

if every month save RM3500,

after 12 months,

I will have 12xRM3500 = RM42,000.

This year even though I got shares investment,

but since my capital was still low,

so even a 15% return also not much,

can be ignored.

By having RM42,000 capital,

I can use the 3rd weapon which is SMF.

(SMF = Share Margin Financing)

SMF don't have to use so much,

just 30% is enough,

so around RM18,000.

As a result,

Asset=RM60,000.

Which RM42,000 is equity, RM18,000 is debt.

2nd year,

every month save RM3500 again,

so by adding another RM42,000...........

Asset = RM102,000.

Which RM84,000 is equity, RM18,000 is debt.

Then return of investment of RM60,000 from last year is 15%,

so is 0.15x60k = 9k, earned RM9000 from investment.

Thus,

Asset = RM111,000.

Which RM93,000 is equity, RM18,000 is debt.

By having more equity,

more SMF can be used,

but still maintain at 30% ratio,

so around RM22,000 from SMF.

As a result,

Asset = RM133,000.

Which RM93,000 is equity, RM40,000 is debt.

3rd year,

continue to save RM3500 every month,

so will have another RM42,000 capital, net worth 6 figures.

Asset = RM175,000.

Which RM135,000 is equity, RM40,000 is debt.

Then return of investment of RM133,000 from last year is 15%,

so 0.15x133k = 20k, earned RM20,000 from investment.

Thus,

Asset = RM195,000.

Which RM155,000 is equity, RM40,000 is debt.

Since already have RM195,000,

so another RM5000 from SMF,

it will become RM200,000.

If want to continue to accumulate more wealth,

SMF 30%,

another RM25,000 can be used from SMF.

As a result,

Asset = RM220,000.

Which RM155,000 is equity, RM65,000 is debt.

During the early days of my investment,

I used high income, reasonable shares investment and SMF these 3 weapons to accumulate my wealth.

Of course,

this was my method,

it might not be suitable for other people.

Every month save RM3500??

A lot of people like to hypnotize themselves for not being able to do it.

SMF 30%??

A lot of people reject and scared of debt.

Investment return 15% ??

I guess a lot of people will accept this,

since there wasn't any bearish market lately,

and most of the people earned more than 15%~

That's all about my 3 weapons.

How many weapons are you holding to face the shares market?

Are those weapons really suitable for you?

Investment is about doing own thinking, making own decision.

Thanks for reading.

I don't provide any buying/selling suggestion above,

please make your own investment decision and be responsible with it.

please make your own investment decision and be responsible with it.

Recent articles :

HARTALEGA latest financial report

Year 2018 version:the consequence of long term investment

AEONCR latest financial report

Waiting and waiting, when will the stock market crash?

AEON 2nd quarter 2018 financial report

Other links:

List of articles of year 2018

List of articles of year 2017

My investment return for year 2017

My self-introduction article

My Twitter : @TheCellist86

Subscribe to:

Comments (Atom)